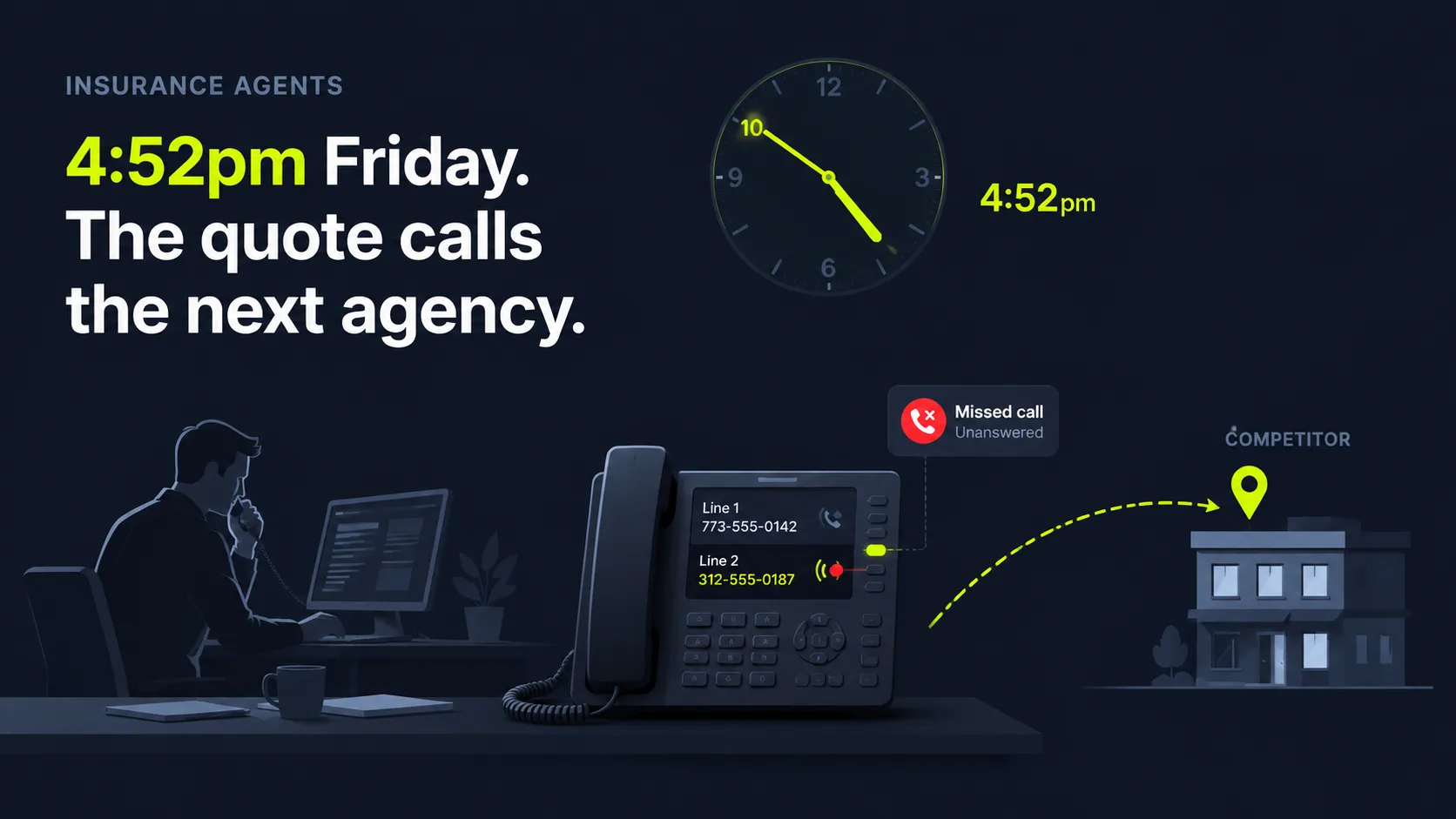

Why do insurance agents lose policies to missed quote and service calls?

Agents lose policies because callers won't wait and won't try twice. The leak is right there in the call data: 27% of inbound calls to service businesses go unanswered, and fewer than 3% of voicemail callers leave a message, per Invoca (2024). An older 30-day audit put unanswered small-business calls near 62%, per 411 Locals (2016). A shopper comparing rates rarely circles back. The agency that answers writes the policy.

Here's the part most owners underrate. The phone is a high-intent lead source, not an interruption. 66% of small businesses rate inbound phone calls as a good or excellent lead source, the top-rated channel ahead of online forms, in-person, and email, per a long-cited BIA/Kelsey report (2014). Someone who picks up the phone to ask about a quote isn't browsing. They're at the buying stage, wallet half-open.

So speed isn't a nicety. It decides who binds the policy. Firms that contact a lead within an hour are nearly 7 times more likely to qualify it than those who wait even an hour longer, and more than 60 times more likely than firms waiting 24+ hours, according to Harvard Business Review (2011). A producer trapped in a closing meeting can't beat that clock. An agent that picks up on the first ring can.

And no, voicemail won't save the lead. For service businesses, fewer than 3% of callers pushed to voicemail actually leave a message, per Invoca (2024). A shopper who hits your voicemail box has usually already dialed the next agency on the list before your greeting finishes. The beep is the sound of the lead leaving.

Citation capsule: For service businesses, 27% of inbound calls go unanswered and fewer than 3% of voicemail callers leave a message, per Invoca (2024). Firms that respond within an hour are nearly 7 times more likely to qualify a lead than those that wait, per Harvard Business Review (2011). Every missed quote call is a high-intent insurance prospect a competitor can catch.

Working with agencies, [PERSONAL EXPERIENCE] we noticed the worst drops happen during the most productive hours. Producers sit buried in renewals, claims follow-ups, and review meetings, exactly when a cold shopper calls for an auto or home quote. The agency that answers in that window writes the easy new business a busy office never even hears ring. Think about how much of that is happening to you right now, on a line nobody is watching.

It also helps to understand the broader pattern in our overview of how missed calls cost service businesses revenue.

How does SkoreFlow capture quote requests and qualify new prospects?

SkoreFlow's AI voice agent answers in about 0.4 seconds and runs a structured intake script built for insurance, so it captures the same details a producer would, on every call, without fatigue. A traditional answering service takes a message and leaves you to call back. This one qualifies the prospect and books the producer callback while the caller is still on the line. Because firms that respond within an hour are nearly 7 times more likely to qualify a lead (per Harvard Business Review, 2011), answering instantly is the single highest-impact move an agency can make.

The intake flow follows a consistent order:

- Greet and identify the need. The agent confirms your agency name and asks what the caller needs (new quote, policy change, billing, ID card, or a claim).

- Capture contact details. Full name, phone, email, and best time to reach them, recorded verbatim.

- Identify the coverage line. Auto, home, renters, life, commercial, or umbrella, so the lead routes to the right producer.

- Collect quote-starter details. For auto: vehicle year, make, model, and drivers. For home: address, property type, and approximate age or value. Enough to start the quote, not a full application.

- Qualify intent and timing. Current carrier, renewal or expiration date, and whether they're shopping a rate or filling a coverage gap.

- Flag urgency. It separates a routine quote request from a same-day need, like proof of insurance required to close on a car or home.

- Book a callback or appointment. It offers open slots and schedules a callback or meeting with the producer for hot prospects.

- Route and notify. A clean lead summary lands on your phone or calendar within seconds, with booking handled through tools like Google Calendar. Direct sync to insurance agency management systems is on request [CONFIRM].

Here's the win that surprises owners. [PERSONAL EXPERIENCE] In our experience setting up insurance intake scripts, the biggest lift comes from collecting the coverage line and quote-starter details before a producer ever calls back. When the agent captures vehicle info or property basics up front, your producer opens the rater already knowing what to quote. No more burning the first five minutes of a callback re-gathering basics the prospect already gave once. That saved time compounds across every quote your office writes.

Citation capsule: Firms that contact a lead within an hour are nearly 7 times more likely to qualify it, and over 60 times more likely than those waiting 24+ hours, per Harvard Business Review (2011). An AI agent answering on the first ring collects quote-starter details and books the producer callback while the shopper is still on the line.

| Response window | Relative odds of qualifying the lead |

|---|---|

| Within 1 hour | About 7x more likely than waiting just over an hour |

| Waited 24+ hours | Baseline; over 60x less likely than the 1-hour group |

Different verticals need different intake scripts, so it helps to compare answering service options by industry, including legal, accounting, real estate, and mortgage.

How does after-hours first-notice-of-loss and claims intake work?

It works by giving every after-hours caller a calm, structured intake instead of a voicemail box, then escalating the urgent ones fast. After a missed response window, 56% of customers immediately try another channel and 28% abandon entirely, according to Nextiva (2025). A policyholder calling about a car accident at 9pm needs a steady voice on the line, not a beep.

Picture that 9pm call. Glass on the shoulder of the road, hazard lights ticking, a shaken driver fumbling for the policy number. Claims and emergencies don't keep office hours. A homeowner with a burst pipe, a driver in a fender-bender, or a small-business owner staring at water-stained inventory tends to call the moment it happens, which is rarely 9-to-5. Consider an analogy from other local services: restaurants take 51% of their calls after 5pm, per BrightLocal (2019). Insurance call timing differs, but loss events clearly happen nights and weekends, and the cost of a missed window is universal: 56% of customers try another channel after one, per Nextiva (2025).

The agent handles first-notice-of-loss the way your office would. It calmly takes the policyholder's name, policy number if known, date and time of loss, type of loss (auto, property, liability), a short description, and whether anyone is injured or property is at risk. Then it follows your escalation rules. No pause, no on-call number to dig up, no morning surprise.

What counts as urgent versus routine after hours

Urgency separates the calls that need a person tonight from the ones that can wait for morning. An injury, an active water leak, a vehicle that isn't drivable, or a liability situation gets escalated immediately to your on-call adjuster or producer per your rules. A routine claim question, a fender-bender already handled, or a policy-detail check gets a recorded report and a next-business-day callback. Nobody is woken up for an ID-card question, and nobody waits until 8am with a flooding basement.

How escalation reaches the right person

Escalation follows your routing logic, not a one-size queue. The agent can connect a live call, send an instant text and email summary, or trigger an on-call rotation so the right person hears about an urgent loss within seconds. Every after-hours call produces a structured record, so nothing depends on someone remembering to check voicemail at 7am.

Now here's the reframe that changes the math. Most agencies treat after-hours claims as a service cost to minimize. [UNIQUE INSIGHT] We've found it's actually a retention and referral engine. The policyholder who reaches a calm, competent intake at 9pm after an accident remembers it at renewal, and tells friends at the next backyard cookout. The one who hit voicemail remembers that too, and tells the same friends. One late-night call can swing a household's loyalty for years. Which side of that story do you want to be on?

Citation capsule: After a missed response window, 56% of customers immediately try another channel and 28% abandon entirely, per Nextiva (2025). An AI answering service takes after-hours first-notice-of-loss details on every call and escalates injuries, active leaks, and liability events to the on-call adjuster within seconds.

This is the core reason 24/7 coverage protects after-hours revenue for any service business that fields urgent calls.

AI vs. traditional answering service for insurance agents: which fits your agency?

The core trade-off is coverage versus headcount: AI answers every call instantly at a flat cost, while a traditional live service offers human voices at a premium with limited capacity, often metered per minute. Live virtual receptionist plans at one national provider run from $250/month for 50 minutes to $1,725/month for 500 minutes, per Ruby's pricing page (2026), which works out to roughly $3.45 to $5.00 per receptionist-minute.

Both models beat voicemail. The real question for an agency is which mix of cost, capacity, and insurance-specific intake fits your call volume and lines of business.

| Factor | AI answering service for insurance agents | Traditional live answering service |

|---|---|---|

| Availability | 24/7, no hold time, answers on first ring | Business hours or after-hours desk; possible hold queue |

| Quote intake | Structured capture of coverage line, vehicle/home, and contact every call | Depends on agent training and script adherence |

| Claims / first-notice-of-loss | Consistent FNOL capture with rule-based escalation | Varies by agent; nuance handled by judgment |

| Cost signal | Typically below live plans; AI receptionist tiers from ~$95/mo, per Smith.ai (2026) | $250-$1,725+/mo at ~$3.45-$5.00/min, per Ruby (2026) |

| Per-minute fees | Flat plans, no per-minute metering | Often metered per minute |

| Concurrent capacity | Unlimited simultaneous calls; no busy signal | Limited by staffed agents on duty |

| Consistency | Same intake script every call and shift | Varies by agent and shift |

| Human escalation | Routes urgent claims and hot prospects to your line | Live agent judgment for nuance |

| Best for | After-hours coverage, quote capture, tight budgets | Owners wanting a human voice on every call |

Most owners frame this as AI or human. [UNIQUE INSIGHT] We've found the sharper frame is AI plus human escalation. The AI captures the routine quote and the after-hours FNOL a live desk would charge per minute to handle, then hands the genuine emergency, like an injury claim, straight to your on-call person. You stop trading coverage for judgment, and you stop paying $4 a minute for ID-card requests.

There's a second difference that matters more than price. A live service like Ruby takes a message and leaves you to call the shopper back, by which point they've often bound elsewhere. SkoreFlow's agent qualifies and books on the call. It captures appointments, not just messages, so a hot quote prospect leaves the call already scheduled with a producer. That's the gap between hearing about a lead and owning it.

| Model | Entry price | Pricing structure |

|---|---|---|

| AI receptionist | From about $95/month | Flat plan, no per-minute metering |

| Live virtual receptionist | $250 to $1,725+/month | About $3.45 to $5.00 per receptionist-minute |

Citation capsule: Live virtual receptionist plans cost roughly $3.45 to $5.00 per receptionist-minute, derived from Ruby's published 2026 pricing ($250/mo for 50 minutes to $1,725/mo for 500 minutes). AI answering tiers, starting near $95/month per Smith.ai (2026), let agencies capture every quote and claims call for far less, with no per-minute fees.

What does it cost, and what is the ROI?

Pricing spans a wide band, but the ROI math is simple: one bound policy often pays for months of coverage. Industry pricing for virtual receptionist services runs about $50-$300/month for AI and $300-$2,000+/month for human services, per CloudTalk (2025). Against the lifetime value of a single new household, that monthly cost is a rounding error.

The return comes from the calls you currently lose. Remember the data: 27% of service-business calls go unanswered and fewer than 3% of voicemail callers leave a message, per Invoca (2024), with an older audit putting unanswered small-business calls near 62%, per 411 Locals (2016). Hiring a receptionist instead means a median wage of $37,230 a year before benefits, per the U.S. Bureau of Labor Statistics (2024), and one person still can't cover nights, weekends, and a quote surge at once. The AI covers every call around the clock for a fraction of that.

Here is what the leak actually looks like in dollars.

Illustrative example (industry-based scenario, not a real client): Picture an agency missing 12 quote calls a week, or roughly 624 a year. Voicemail recovers almost none of them, since fewer than 3% of callers leave a message, per Invoca (2024). Now anchor the value. A single first-year life policy commonly pays 55% to 120% of first-year premium in commission, per ACLI data via NerdWallet (2024). On a modest $1,200 annual premium at a 70% first-year rate, that one policy is worth about $840 in commission.

Now run the recovery math. Suppose the agent answers those 624 missed calls and binds just 5% of them, about 31 policies. At roughly $840 each, that is around $26,000 in first-year commission. Compare that to an AI answering plan in the $50 to $300/month band, per CloudTalk (2025), or $600 to $3,600 a year. Even at the low end of binding and the high end of plan cost, the recovered premium pays for the service many times over. That spread is the whole argument. Run your own numbers with our Missed Call Revenue Calculator.

The premium, rate, and bind percentages above are illustrative assumptions, not measured client results. Only the commission range and pricing band are sourced.

Citation capsule: Virtual receptionist pricing runs about $50-$300/month for AI versus $300-$2,000+/month for human services, per CloudTalk (2025). Against a median in-house receptionist wage of $37,230/year (BLS, 2024), an AI answering service covers every quote and after-hours claims call at a fraction of the cost.

| Line item | Annual figure |

|---|---|

| Missed quote calls recovered (624 at 5% bind) | About 31 policies |

| First-year commission per policy ($1,200 premium at 70%) | About $840 |

| Recovered first-year commission | About $26,000 |

| AI answering-service cost ($50 to $300/mo) | $600 to $3,600 |

Why do insurance agents choose SkoreFlow?

Agents choose SkoreFlow because it closes the exact gap the data exposes: a live answer on every call, structured quote intake, consistent first-notice-of-loss capture, and instant escalation when a claim is urgent. With 27% of service-business calls going unanswered and almost no one leaving a voicemail, per Invoca (2024), simply answering well is a competitive edge most agencies haven't claimed yet.

Remember that nervous driver at the lot, and the shaken one at 9pm? The approach respects how people actually feel about AI on those calls. 64% of customers would prefer companies didn't use AI in customer service, and their top concern is that it will get harder to reach a person, per Gartner (2024). So the SkoreFlow agent sounds natural, never traps a caller in a menu, and hands off to a human the moment a claim or prospect needs one. That matters most in insurance, where someone calling after a loss needs to feel heard before they need a form filled out.

The offer is built to be low-risk, on purpose. Setup goes live in about 48 hours, intake runs TCPA-aware, and the work is backed by a guarantee: book 5 qualified appointments in the first 30 days or your setup fee is refunded. Plans start at $197/month for lower call volumes and scale up as your inbound grows, so the cost stays well under a live virtual receptionist. You're not betting on a promise. You're protected if the first month doesn't deliver.

We don't publish invented testimonials or named client results. What we will say plainly: the agencies that benefit most are the ones currently sending quote calls and after-hours claims to voicemail. Plug the leak first, then optimize. That order tends to produce the fastest, most honest wins.

Citation capsule: 64% of customers would prefer companies didn't use AI in service, and their top concern is that it gets harder to reach a person, per Gartner (2024). An insurance agent that answers naturally and escalates urgent claims and hot prospects to a human resolves that objection while capturing the calls voicemail loses.

Stop sending quote and claims calls to voicemail

The pattern in the data is hard to ignore: a large share of small-business calls go unanswered, almost no one leaves a voicemail, and the agency that responds first usually binds the policy. An AI answering service for insurance agents closes that gap by answering every call, capturing quote requests, taking after-hours first-notice-of-loss reports, routing service calls, and escalating urgent claims to the right person.

So you don't have to choose between serving current clients and capturing new ones. Let the agent catch the quote calls and the 9pm claims, then hand you the work that needs a producer. Want to see what unanswered calls are costing you? Book a Free Call Audit. It's a 20-minute, no-pressure call where we map where policies are slipping and what capturing them would be worth, and you walk away with the number whether or not you hire us. Prefer to run it yourself first? Start with our Missed Call Revenue Calculator. Either way, the leak stops being invisible.

Written and reviewed by Maksim Skorokhod, Founder of SkoreFlow, who builds AI answering and voice automation for small service businesses. Last reviewed: 2026-06-07.